When you sell or use stock, the order in which you record that movement affects your costs, your reporting, and in some industries, your compliance.

FIFO and LIFO are two of the most common inventory valuation methods. They answer a simple but important question: when you remove a unit from stock, which unit's cost do you record?

The answer changes depending on how your business operates.

What FIFO Means

FIFO stands for First In, First Out.

The oldest stock is used or sold first. When you record a sale or consumption, you assign the cost of the earliest batch purchased.

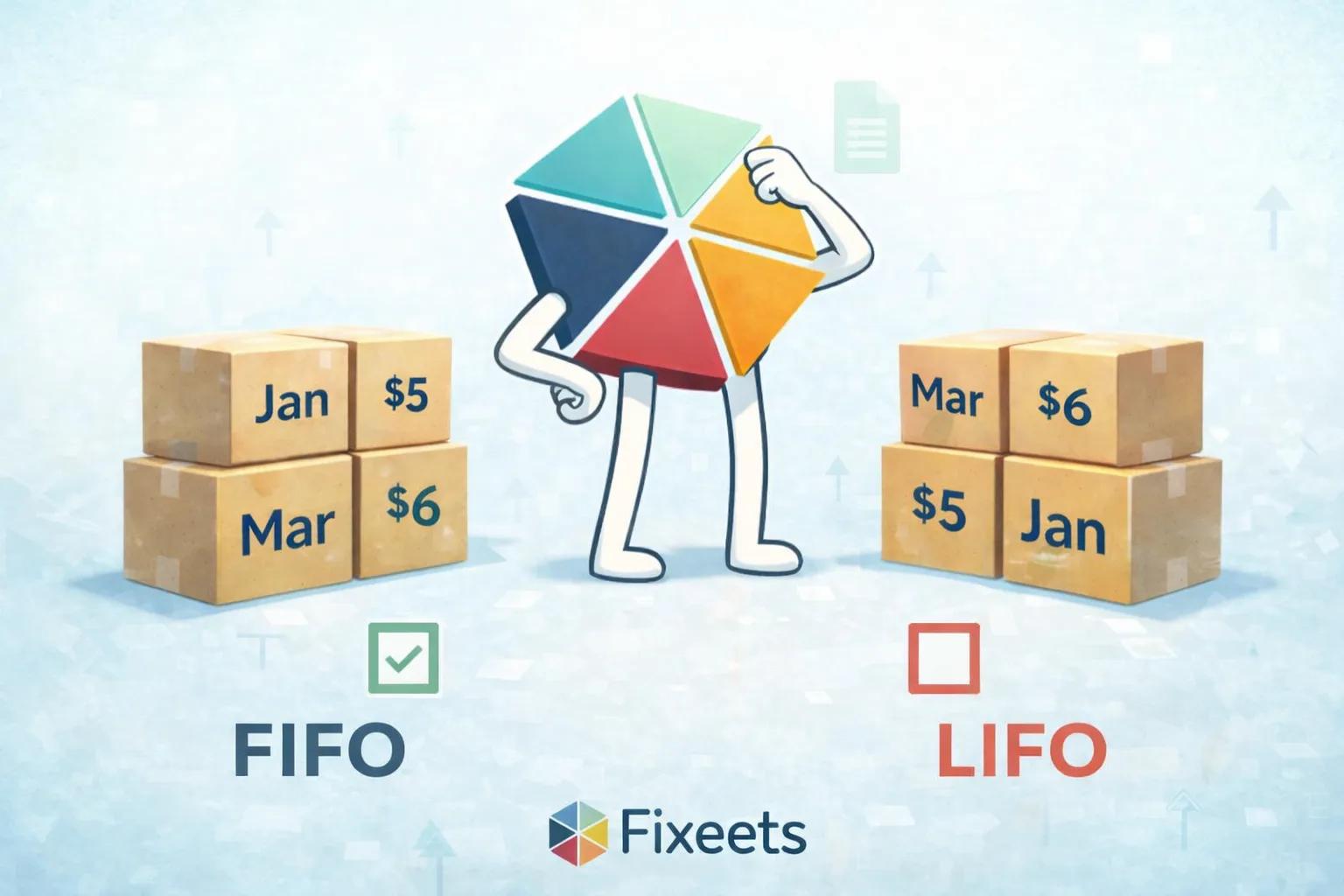

Example: A pharmacy receives 100 units of a medication in January at $5 each, then another 100 units in March at $6 each. Under FIFO, the first units sold are costed at $5. Once the January batch is cleared, the March batch takes over.

This method reflects how most businesses actually move physical stock. Older items leave first. Newer items wait.

FIFO is widely accepted under both IFRS and US GAAP, making it the default method for most businesses operating internationally.

What LIFO Means

LIFO stands for Last In, First Out.

The newest stock is treated as the first to be used or sold. When you record a movement, you assign the cost of the most recently purchased batch.

Example: Using the same pharmacy scenario, under LIFO the units sold first are costed at $6 (the March batch), even if the January stock is physically still sitting on the shelf.

LIFO is only permitted under US GAAP. It is not accepted under IFRS, which means businesses operating outside the United States or reporting under international standards cannot use it.

In practice, LIFO is primarily used for accounting and tax purposes in the US, not because it reflects physical stock movement.

Key Differences at a Glance

| Parameters | FIFO | LIFO |

|---|---|---|

| Cost assigned on sale | Oldest batch | Newest batch |

| Accepted under IFRS | Yes | No |

| Accepted under US GAAP | Yes | Yes |

| Reflects physical flow | Usually yes | Usually no |

| Best for perishables | Yes | No |

| Common in practice | Very common | Limited to US |

Which Method Works for Small Businesses?

For most small businesses and SMEs, FIFO is the practical and safe default.

If you sell or use physical goods that expire, degrade, or go out of date, FIFO also matches how you should be moving stock. Older items should leave first. FIFO keeps your accounting aligned with your actual operations.

LIFO is mostly relevant if you are a US-based business with a specific tax strategy, or if your accountant has recommended it for your cost structure. Even then, it requires careful tracking because the costs on paper no longer reflect which units physically left your shelves.

If you are outside the United States, LIFO is not an option under IFRS. FIFO is your method.

How This Applies to Inventory in Google Sheets

Most small teams tracking inventory in Google Sheets do not think about FIFO or LIFO explicitly. They record what came in and what went out.

But if you are costing your stock movements or running any financial reporting from your inventory data, the method you apply determines your cost of goods sold and your remaining stock value.

Structured inventory tools make this easier. Fixeets Inventory Management tracks stock movements inside Google Sheets with controlled data entry, so each movement is recorded accurately. Teams can apply consistent costing logic without building it manually across formulas.

This is especially useful for businesses that also manage maintenance and spare parts inventory, where batch tracking and reorder accuracy directly affect operations.

If you are still setting up your inventory structure, the step-by-step Google Sheets inventory guide covers the foundations before you layer in costing logic.

The Practical Answer

Most small businesses should use FIFO. It reflects real stock movement, it is accepted everywhere, and it keeps your records honest.

LIFO is a narrower tool for specific tax contexts in the US. Unless your accountant has given you a clear reason to use it, FIFO is the simpler and more defensible choice.

What matters more than which method you choose is that you apply it consistently, track each movement accurately, and make sure your team records stock the same way every time.

That consistency is what good inventory management actually depends on.

For the fundamentals around costing methods - what inventory management involves, how to choose a system, and how to run it well - our complete inventory management guide covers the full topic in one place.

Key Takeaways

- FIFO (First In, First Out) assigns the oldest batch cost when recording a sale or consumption, reflecting how most businesses actually move stock physically

- LIFO (Last In, First Out) is only permitted under US GAAP and is not available to businesses reporting under IFRS

- For most small businesses, FIFO is the practical and safe default: it matches physical stock flow and is accepted everywhere

- LIFO is primarily relevant for specific US-based tax strategies, not because it reflects real inventory movement

- Consistent application of whichever method you choose matters more than which method you pick. Structured tools help ensure that consistency across the team